SanDisk has been one of the standout performers in the stock market in 2026, drawing attention from investors and analysts alike. After spinning off from Western Digital in early 2025, SanDisk re-entered the public markets as an independent memory and flash storage company focused on advanced NAND technology and solid-state drives (SSDs) — a sector experiencing strong long-term demand driven by data-intensive applications like AI, cloud computing, and hyperscale data centers.

Company Background and Market Position

Founded in 1988 and previously part of Western Digital, SanDisk has deep roots in flash memory innovation. In February 2025, the company completed its spin-off from Western Digital, relisting on the NASDAQ under the symbol SNDK to pursue focused growth in flash and SSD technologies. This strategic separation positioned SanDisk to capitalize directly on high-growth markets without being tied to the broader HDD-centric operations of its former parent.

SanDisk’s product portfolio includes high-performance SSDs for data centers, enterprise applications, embedded storage, and consumer devices. New technologies like its BiCS8 flash architecture and enterprise-grade SSD product lines such as Stargate are key drivers of demand — especially from cloud service providers and hyperscalers.

Recent Financial Performance and Growth Metrics

SanDisk’s most recent financial results reinforce its growth trajectory. In the first quarter of fiscal 2026, the company reported revenue of $2.31 billion, a sequential increase of 21%, with non-GAAP earnings per share (EPS) significantly beating expectations. Data center revenue — a key growth segment — rose by 26% sequentially, and SanDisk exited the quarter in a net cash position, enhancing its financial flexibility.

Analysts also believe technology adoption will continue to support future performance. Industry projections show that investment in data centers, AI infrastructure, and advanced memory solutions could grow substantially through the remainder of the decade, potentially boosting SanDisk’s addressable market.

S&P Global Ratings recently revised its outlook for SanDisk’s revenue to grow toward $10 billion in fiscal 2026, up from about $7.3 billion in 2025, fueled by favorable pricing and demand trends in the NAND market. The company has also focused on debt reduction, improving leverage and free cash flow expectations.

Bullish Factors: What’s Driving Optimism

Strong Demand Environment

The global memory and storage market continues to benefit from expanded use of AI, cloud computing, and hyperscale data infrastructures. As organizations build out capabilities to support large-scale models and data storage needs, demand for high-capacity, efficient flash memory grows. SanDisk’s products are positioned to tap directly into this trend.

Analyst Support and Stock Momentum

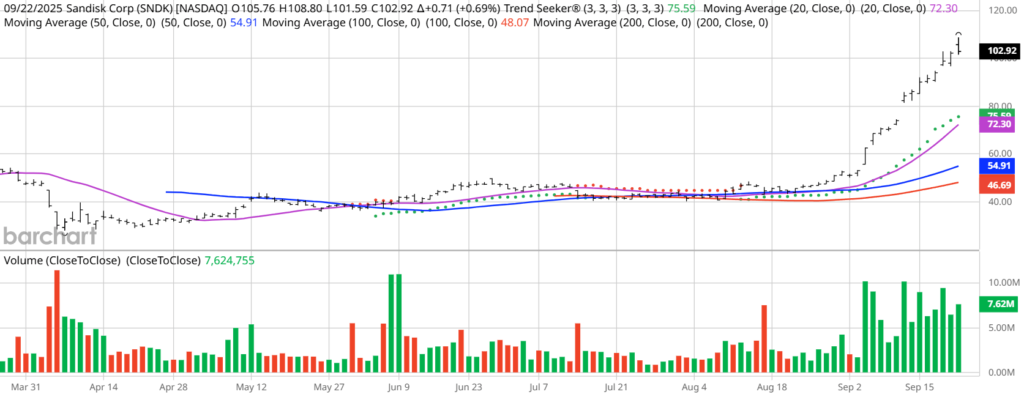

SanDisk has generated significant stock price appreciation since its re-listing, with strong year-to-date gains driven by rising expectations for memory technology demand. Some analysts have issued price targets significantly above current trading levels, while many maintain Buy or positive ratings based on long-term growth prospects supported by structural industry demand.

Supply–Demand Dynamics in NAND Flash

The NAND flash market — the core of SanDisk’s business — is characterized by periodic supply constraints and cyclical pricing trends. When demand outpaces supply, pricing power and margins can improve, benefiting manufacturers like SanDisk. Several analysts believe that supply growth trends remain moderate relative to strong demand driven by AI and storage expansion, creating tailwinds for pricing and profitability.

Risks and Cautions for Investors

Despite strong performance, potential investors should consider several risk factors. High current valuations — a by-product of the stock’s rapid rise — mean that future returns may be more modest if growth expectations are already priced in. Some analysts have projected limited upside from current levels based on price targets at or near the existing share price, raising concerns about valuation risk.

Additionally, memory markets can be cyclical, and shifts in global supply, competitive pressures (including from other major memory makers), and macroeconomic conditions can influence pricing, demand, and profitability over time.

Is SanDisk Stock a Good Buy in 2026? Final Thoughts

Whether SanDisk stock is a good buy in 2026 depends on an investor’s risk tolerance and investment horizon. On one hand, the company’s strong financial performance, improving fundamentals, and alignment with high-growth technology trends position it as a compelling long-term growth play in the tech sector. On the other, near-term valuation risk and broader market cyclicality warrant cautious evaluation.

Investors seeking exposure to AI-driven storage demand and flash memory growth may find SanDisk’s story attractive, especially given its recent expansion and improving financial metrics. However, balancing optimism with disciplined analysis — including monitoring supply dynamics, competitor moves, and overall market conditions — remains essential in making an informed investment decision.

#SanDiskStock #SNDK #StockAnalysis #StockMarket #Carrerbook#Anslation#Investing2026 #TechStocks #GrowthStocks #SemiconductorStocks #MemoryStocks #NANDFlash #DataCenterStocks #AITechnology #MarketOutlook #StockForecast #FinancialAnalysis